Military families navigate unique financial terrain—frequent PCS moves, sudden deployments, and tight budgets all shape how and where you live. If you're considering buying a home, selecting the right mortgage term is more than just a numbers game—it’s a strategic decision that affects your financial flexibility and long-term wealth. In this post, we’ll break down the differences between 15- and 30-year mortgages, run sample calculations across various loan amounts, and highlight the pros and cons of each option to help you choose what’s best for your mission at home.

Understanding the Basics

At its core, a mortgage is a long-term loan used to buy a home. The two most common terms are:

- 15-Year Mortgage:

- Shorter duration, meaning the loan is paid off in 15 years.

- Higher monthly payments, but you generally enjoy a lower interest rate and pay significantly less interest over the life of the loan.

- 30-Year Mortgage:

- Longer duration, spreading the cost over 30 years.

- Lower monthly payments, offering more cash‑flow flexibility, though you’ll typically pay more in total interest over time.

For military families, making a choice should depend on your current income stability, plans for relocation, and the amount of cash flow needed to manage other household or deployment expenses.

Breaking Down the Numbers

Let’s explore an example, using the August 2025 median price of a starter home in the United States. The following illustrations use the median interest rates as of mid-August 2025. (Mortgage rates fluctuate often, so check with your lender or a financial advisor for current rates in your area.)

Example: A $396,000 Home Loan

For our examples, we assume the median rates as of mid-August:

- A 30‑year mortgage with an annual interest rate of 6.57%.

- A 15‑year mortgage with an annual interest rate of 5.75% (often, lenders offer a discount on shorter terms).

Estimated Payment Calculations

| Mortgage Term | Interest Rate | Monthly Payment | Number of Payments | Total Interest Paid |

| 30‑Year | 6.57% | $2,521 | 360 | $511,647 |

| 15‑Year | 5.75% | $3,288 | 180 | $123,685 |

How are these numbers derived? For a 30-year mortgage, the principal and interest of approximately $1,592 is calculated using the standard amortization formula. The 360 payments total $907,647. Subtracting the $396,000 principal, the total interest costs $511,647. In contrast, for a 15-year term with a slightly lower rate, the monthly payment is higher at $3,288, but with only 180 payments, the overall interest is only $195,917. A 30-year loan’s lower monthly payment provides greater flexibility, but you will pay more than twice the interest of a 15-year loan.

These payments include principal and interest only (P&I), but your lender may require you to fund an escrow account to include local taxes and insurance in your monthly payments (PITI). Remember to budget for escrow each month; it remains the same regardless of a 15- or 30-year mortgage, but may increase over time as taxes and property insurance rates rise.

Pros and Cons for Military Families

When choosing between a 15 and 30-year mortgage, consider how each aligns with your lifestyle and financial priorities:

15-Year Mortgage

- Advantages:

- Lower Total Interest: The rapid repayment schedule greatly reduces overall interest costs.

- Faster Equity Building: With the home paid off in half the time, you build home equity more quickly—which can be beneficial if you plan to sell when back home or during a transition.

- Potential Interest Rate Advantages: Lenders often offer lower rates on 15-year loans due to reduced risk.

- Disadvantages:

- Higher Monthly Payments: The cost per month is higher, which may reduce your budget flexibility for emergencies, frequent moves, or other unexpected expenses.

- Less Cash Flow Flexibility: With more of your income committed to housing, there’s reduced capacity for other investments or saving for future deployments.

30-Year Mortgage

- Advantages:

- Lower Monthly Payments: More manageable payments can ease budgeting, particularly when income might fluctuate during relocations or long-term assignments.

- Increased Cash Flow: Lower payments allow you to invest in other areas like education, retirement, or emergency funds.

- Flexibility for Frequent Moves: If you expect to move often, a longer term can be less taxing on your monthly budget, even if you pay off the balance sooner through prepayments.

- Disadvantages:

- Higher Total Interest: While monthly payments are lower, stretching the repayment over 30 years means you’ll pay significantly more interest overall.

- Slower Equity Build‑Up: Home equity accumulates at a slower pace, which can be a disadvantage if property values fluctuate or if you plan to move frequently.

- Potential for Overstretching Monthly Budgets: Even though the payment is lower, a longer commitment may affect your overall financial planning, especially when balancing multiple moving or deployment costs.

A Note on VA Loans

Many military families qualify for a VA loan, which often comes with competitive rates, no down payment options, and other benefits. These terms can sometimes offset some drawbacks of either mortgage option, ensuring you benefit from the best possible rate regardless of the chosen repayment period. Always check the specific benefits available to you as a service member when considering your mortgage choices.

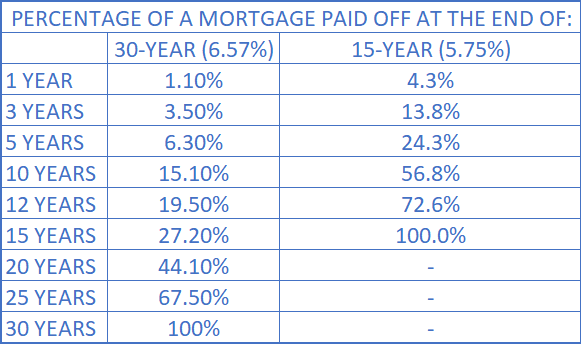

How Fast Will My Home Be Paid Off?

This chart illustrates how much of your mortgage balance is paid off at various points throughout the mortgage life cycle. The higher payment of the 15-year mortgage builds equity faster!

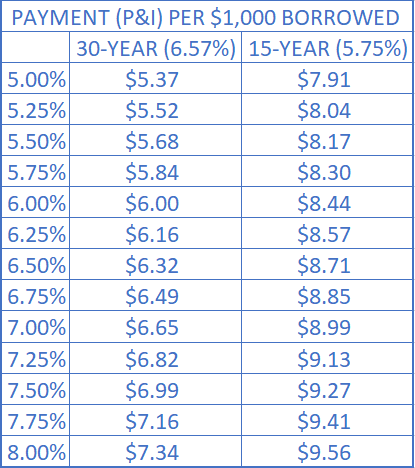

How to Estimate Your Payment

This chart shows the approximate payment per $1,000 borrowed for 15 and 30-year mortgages using various interest rates. Divide the total amount borrowed by 1,000 and multiply by the amount per $1,000 for your approximate principal and interest. Example: If you borrow $412,689 at 6.25% for 30 years, multiply 412.689 by $6.16 to find your payment of about $2,542.

Final Thoughts

Deciding between a 15-year and a 30-year mortgage ultimately depends on your current financial situation, long-term goals, and the realities of military life. If you can comfortably handle a higher monthly payment, a 15-year mortgage not only saves you money on interest but also builds equity faster. On the other hand, the flexibility and lower monthly commitments of a 30-year mortgage can be a lifeline when managing unpredictable expenses or frequent relocations.

Before making a decision, consider running your numbers, discussing options with a financial advisor experienced in military benefits, and considering special mortgage products for military families. Balancing immediate cash flow with long-term financial advantages is key.

Explore More with My Military Lifestyle and Finance!